Struggling to find content to share on your social media pages?

Our consumer lifestyle blog, Living Room, offers content including home improvement, market trends, DIY projects, neighbourhood guides and profiles on unique homes. Living Room publishes exciting new content four times a week (with unique French content for our Francophone fans).

While CREA Café is curated specifically to help your business grow and thrive, Living Room content is perfect to share with your clients.

Owned and operated by the Canadian Real Estate Association (CREA), REALTOR.ca is the No. 1 real estate platform in Canada (Comscore, 2020) with MLS® System listings from across the country.

Share this blog with your clients and follow REALTOR.ca on Twitter, Instagram and Pinterest.

You can read the original blog here.

Homeownership has many benefits, including the ability to use your property’s equity as a lending resource.

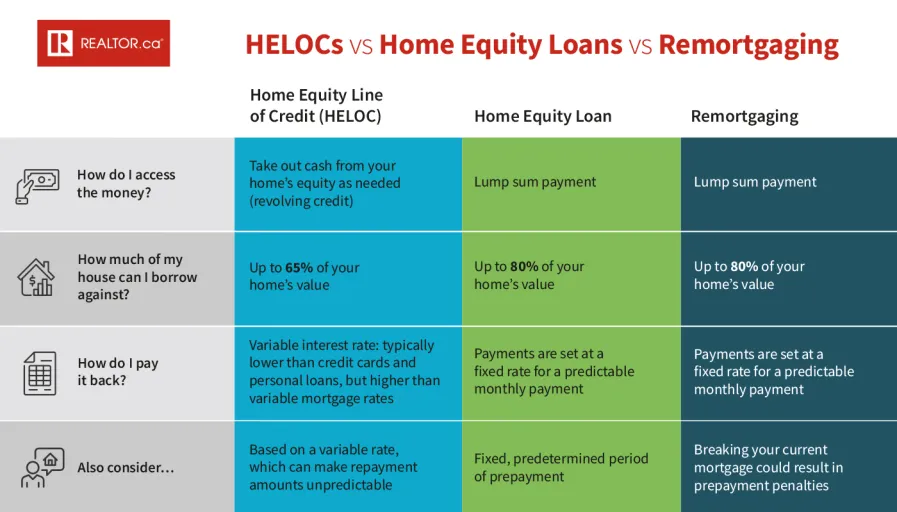

Whether you need funding for a renovation or to consolidate debts, a mortgage holder can access home loans and home equity lines of credit (HELOC) through their property. There’s also the option to remortgage your home, which by breaking your existing mortgage and starting a new one, can provide leftover cash through your home’s equity to pay for large expenses.

If you or your clients are considering employing your home’s equity, here’s what you need to know about HELOCS, home equity loans, and remortgaging.

What is a Home Equity Line of Credit (HELOC)?

If you’d like the flexibility of having a large chunk of change on standby, a HELOC may be an option for you.

A HELOC is a facility on your mortgage that lets you take out cash from your home’s equity as you need it. HELOCs are a type of revolving credit, meaning you can borrow money, pay it back, and borrow the funds again. You can use as much or as little of the HELOC as you want.

In a survey conducted by BNN Bloomberg and RATESDOTCA, 27% of those surveyed said they had a HELOC, and 78% of those respondents stated they had used it. Most participants said they borrowed less than $50,000 on their HELOC.

There are many reasons why someone might make use of their HELOC. According to Elan Weintraub, a mortgage broker and co-founder of Mortgage Outlet, they can be for big expenses such as paying for a vacation or a renovation, consolidating other loans, or for investment purposes. Weintraub has also seen some parents pull money out of their HELOC to help fund their adult child’s wedding or down payment.

“One reason is renovations. I’m going to renovate my basement, it’s $100,000, I pulled the money out of my HELOC and I’m ready to go,” he said. “Another reason is to buy another property. I’m buying a new condo and I need to put $50,000 down when I sign the paperwork or [put down] the deposit.”

A HELOC allows you to access up to 65% of your home’s market value, providing a larger loan amount you wouldn’t likely secure through a credit card or other line of credit. However, your outstanding mortgage loan balance, combined with your HELOC, cannot equal more than 80% of your home’s value.

A HELOC tends to provide a lower variable interest rate compared to credit cards and other personal loans, but is higher than variable mortgage rates. A HELOC also allows borrowers to make interest-only payments, which 8% of HELOC holders tend to do, according to the BNN Bloomberg and RATESDOTCA survey.

“A HELOC is going to be [at] a lower interest rate, and generally you’ll qualify for a much larger amount. It’s unlikely you’re going to get a $100,000 credit card. It’s unlikely you’re going to get a $100,000 unsecured line of credit,” said Weintraub. “But, again, if you’re doing a reno or you want to invest or [do] big things, that’s where you could use a HELOC. So, its two main advantages are lower rates and a larger amount [of money.]”

It’s important to note as interest rates rise, the cost of borrowing also increases, which can affect HELOCs. As home equity lines of credit are based on variable-rate interest, borrowers might be on the hook for higher payments as rates fluctuate in today’s market.

What is a home equity loan?

Although they sound similar to a HELOC, home equity loans are slightly different.

According to the Financial Consumer Agency of Canada, a home equity loan is a one-time lump sum payment. An equity loan starts from $10,000 and can go up to 80% of your home’s value. A home equity loan borrower will pay interest on the entire amount.

Unlike a HELOC, an equity loan isn’t a form of revolving credit, meaning you’ll be required to repay the loan over a fixed, predetermined period, including the principal and interest. However, home equity loan interest rates still tend to be lower compared to credit cards, unsecured personal loans, or lines of credit.

The advantage of a home equity loan is payments are set at a fixed interest rate. If you’re someone who prefers more predictable monthly payments, a home equity loan still allows you to use your home’s equity, but at a more consistent pace.

How does remortgaging work?

If neither a HELOC nor a home equity loan sounds appealing, a homeowner can still extract value from their property’s equity by remortgaging.

Remortgaging, otherwise known as refinancing, involves replacing your existing mortgage with a new one with different terms.

A homeowner may decide to remortgage to take advantage of lower interest rates. Breaking your mortgage before your term ends can open up steep prepayment penalties, which can vary based on several factors, such as the type of interest rate you have. It’s important to understand the size of your pre-payment penalty before you remortgage so you can justify the savings if you switch to a new mortgage.

Remortgaging allows you to access equity in your home when you renegotiate your mortgage terms. A homeowner can tap into 80% of their home’s appraised value as a lump sum, excluding the balance of their current mortgage. Like a HELOC or home equity loan, this money can be used for large expenses, such as to invest, fund a home project, or pay off debt.

Whenever you plan to take advantage of your home’s equity—or make any other changes to your mortgage—there’s a number of factors to consider.

If you intend to move in the near future, inquire if your mortgage is portable, which will allow you to take your existing mortgage along with its current rate and terms from your old property to your new one.

You may also want to ask if there are specific areas of your agreement you can negotiate with your lender, including your mortgage rate. In the initial and renewal stages of a mortgage, it doesn’t hurt to shop around between different companies to find the best rate. In some cases, a mortgage broker will be able to provide added savings to your mortgage—some companies buy down interest rates, which allows them to give up part of their commission from the lender in order to lower their client’s rate. Your mortgage professional will be able to help answer any of these questions.

Whether you opt to use a HELOC, home equity loan, or choose to remortgage, it’s important to understand why and how you plan to use home loans and determine which option works best for you. When talking about loan options with his clients, Weintraub says he determines what their financial needs and goals are and how different products can align with those objectives.

“You have to look at where they are today, what their goals are and then what they have on the table,” said Weintraub.

If you’re looking for mortgage expertise or recommendations on mortgage professionals, recruit the help of a REALTOR® for up-to-date advice.

The information discussed in this article should not be taken as financial or legal advice. This article is for informational purposes only.

Thanks for this. It would have been great if you had included reverse mortgages!

Hi Janet, thanks for your feedback! We have a whole blog post on reverse mortgages. You can find it here: https://www.creacafe.ca/explaining-reverse-mortgages-to-your-clients/